Categories

COVID-19 Insights: 7 Key Takeaways on Consumer Attitude and Future Behaviour

Is your global brand ready for major changes in consumer behavior?

As consumers, we feel and act differently, so businesses have to follow our lead. The focus of many companies has shifted from the profit-driven mindset to value-driven. The main question every business should ask today is: “How can our service or product cater to the changing customer needs?”. For many marketers, advertising and selling in times like these is utterly uncharted territory. However, by listening to the customer, any marketing team will be able to define its position (even in uncertain times like these).

COVID-19 insights: 7 key takeaways on consumer attitude and future behaviour

At boobook, we are committed to bringing consumers’ needs, perspectives, and experiences at the centre of our clients’ businesses. Two months after the crisis hit, we launched a global study with a clear objective to gather as much data as possible to reveal critical insights on changes in consumer behaviour due to COVID-19. The study ran from the end of May until mid-June. Our target group was a nationally representative sample of 4,500 consumers across nine countries (USA, Brazil, France, UK, Germany, Spain, Belgium, China, South Africa) in various stages of the pandemic. The study led to seven key takeaways.

The 7 Key Takeaways on Consumer Attitude and Behaviour

-

Money doesn’t buy happiness

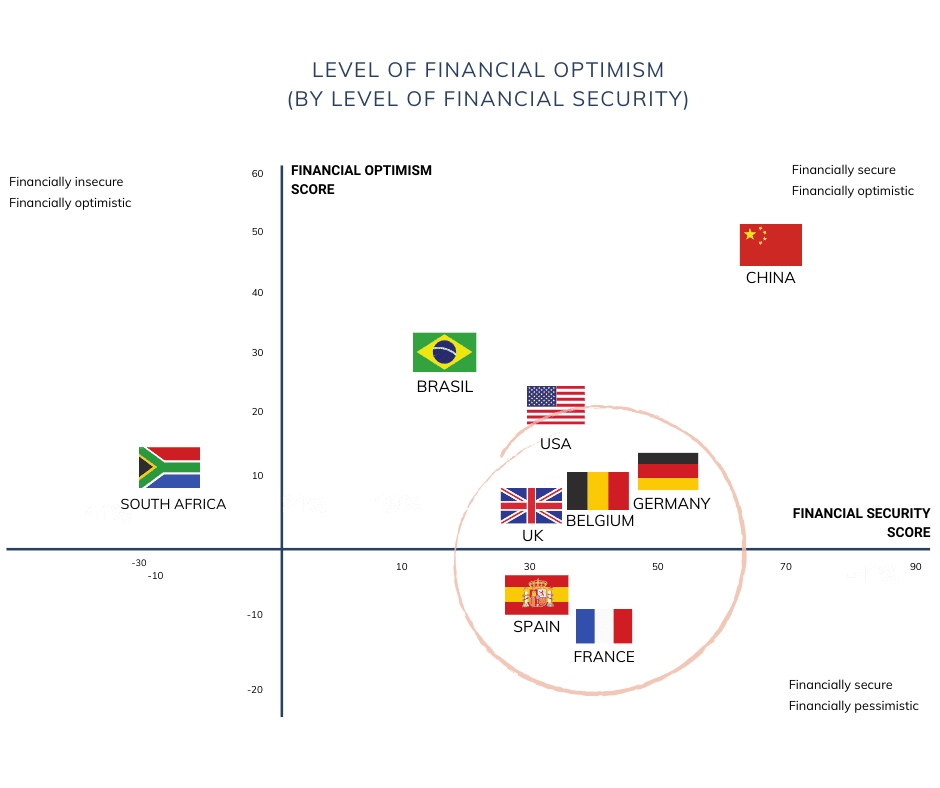

Nearly half the people across the nine markets said that their household income had been reduced in some way because of the pandemic. This impacts directly people’s feelings of financial security in the short to medium-term ability to pay their monthly bills. In markets where there have been higher levels of a reduction in household income, such as South Africa and Brazil, we see higher levels of financial insecurity and concern about the upcoming months.

However, the prediction of how bright the future will be didn’t correlate with the current economic situation. When asked to predict how life will look like after COVID-19, people in countries with the least income stability turned out to be the most optimistic. On the contrary, European countries, with functional social structures and higher living standards, are mostly pessimistic when it comes to finances.

Takeaway: Approach people based on mindset, not only on the financial and pandemic situation in the specific country.

-

Four consumer types emerging out of the crisis. Which one are you?

Based on distinct consumer ways of handling a crisis driven by the financial situation as well as mindset, we defined four segments of consumers:

- Comfortable optimists: the least financially impacted, optimistic about the future, will continue with their purchasing habits

- Considerate spenders: impacted by the crisis, careful with money, optimistic, choosing local, eco and sustainable products

- Cautious wait-and-seers: not heavily affected by the crisis but very pessimistic about the future without any plan or back up

- Financial survivors: struck the hardest by the crisis, pessimistic, constrained to buy cheaper alternatives

Looking at the countries, Europe has many cautious wait-and-seers, while most financial survivors can be found in South-Africa. Considerate spenders are more prevalent in countries with less governmental support. It is clear that someone’s salary cannot explain all behaviour. Mindset and attitude are equally important. It is crucial to understand how customers are coping with the current situation, mindset-wise to successfully engage with them.

Takeaway: Businesses will have to adapt their approach based on these segments where their audience is. It is crucial to understand how customers are coping with the current situation, mindset-wise to successfully engage with them.

-

Saving it Up: Smarter and Long-Term

Despite the crisis, more than half of the consumers saved as much as before or even more. Based on a variety of answers, it’s clear that many consumers, across countries and segments, will pay more attention to saving their money.

The majority of the consumers will use this money for long term saving and investment to secure the future. Short term savings are a second option though less attractive, pointing out that consumers believe this crisis will last for an extended period. Each country drives specific differences in terms of saving behaviour. Still, the biggest driver of how much money people save and what they are planning to do with their savings is linked to the financial security and level of financial optimism of the consumer.

Takeaway: Changes in financial decision making will open many opportunities for financial product providers. But that can also be a threat if the consumer re-evaluates its finances, and he doesn’t see the value anymore in certain investments or his saving plan.

-

Fewer Rather Than Cheaper

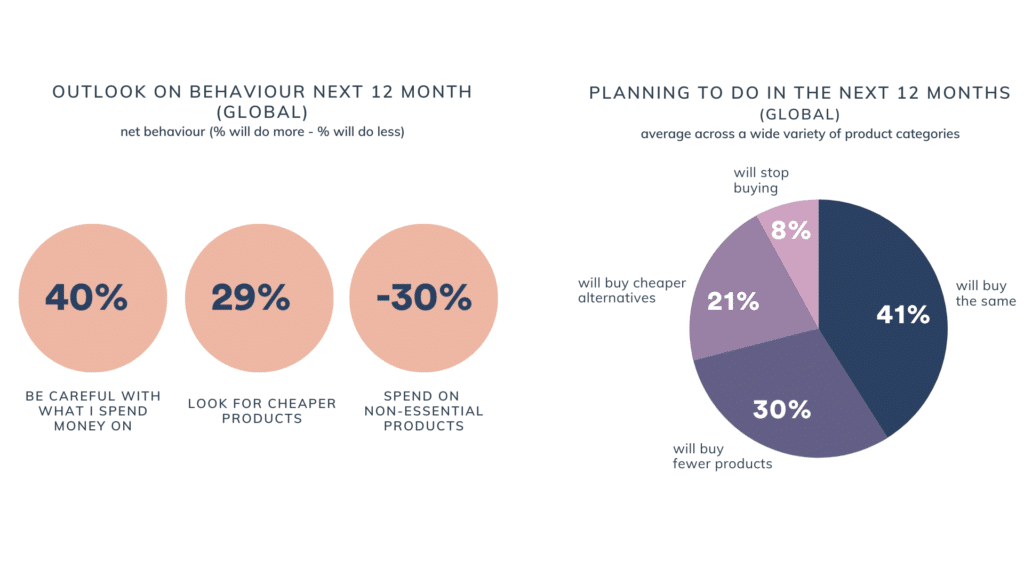

Closely linked to saving more, we also see how people buy more consciously and spend more wisely. When asked what people will do more in the next 12 months, they mention that they will be careful with what they buy rather than buying cheaper products. This reveals how people would rather buy less instead of a downgrade. Even those with increased savings, e.g. will also be more careful about their spending in the current months, as 43% are still going to be cautious about what they spend their money on, and a third will spend less on non-essential products.

However, this doesn’t apply to the “Financial survivors” who are constrained to look for cheaper alternatives.

Takeaway: Keep building positive brand equity. In times like these, it is crucial to give value and quality if you want to stay relevant to your customers.

-

“Clicks & Bricks” Remains the Best Retail Strategy

Even though online shopping is a practical, safe, and easy way of purchasing, the crisis won’t cause a permanent shift to online shopping. Many consumers still enjoy going to stores.

However, there are different underlying tendencies. We identified a group of 20% of respondents who claimed that they would significantly shift their behaviour towards online shopping in the future after the immediate pandemic recedes. This could be because younger age groups typically buy more products online.

Takeaway: Continue building your success on the combination of both an online store and physical shop, integrating the two into a powerful strategy.

-

Family Time is the Best Time

You probably noticed how many shops were out of flour, active yeast, etc. Cooking and baking became an equivalent for family time and enjoying the small things inside your home. It’s not hard to understand how in times of distress and crisis, we generally tend to focus on family experiences, feeling of belonging, togetherness, and care. Another benefit is that cooking at home means we also spend less money.

Even though traveling and socializing are currently at the losing end, it could be only for a short period. When asked how they will treat themselves in the next 12 months, people mostly opted for spending on going out, traveling, fashion, and home & garden.

Takeaway: Create products and services which focus on family experiences, ideally in or near the family home. Virtual health care is on the rise, so might be interesting to offer products or services that provide online healthcare experience.

-

Local Sounds Good, But I’d Rather Pay for Eco, Ethical, and Healthy!

Last but not least, the study shows that the pandemic has changed which key drivers are important in purchase choice. Price, quality, and whether a product is ‘safe for my health’ continue to be the most important drivers while environmental considerations are still most popular among the factors not related to price or quality. However, a brand and shopping environment that is ‘safe for my health’ and ethical have become more important to consumers since the pandemic started.

Takeaway: Keep in mind how the consumer prefers to pay more for eco-friendly/sustainable or ethical than for local products. Ideally, you can offer a product or a service that has all three criteria.

The Study Continues…

The COVID-19 crisis has naturally had a huge impact on many people’s finances and shopping behaviours. Although it looks like the challenges many people have faced will have a long-term impact, there are opportunities for retailers and brands to make the best of a bad situation, ensuring their shops and products are aligned with what people are looking for in the next few months.

With this overview, we just scratched the surface of our global COVID-19 study. On our blog, we present each insight as an individual article where we take a closer look at data.

As a side note, data we gathered now isn’t final. It’s necessary to compare and investigate consumer’s sentiment as the crisis evolves, so we will re-launch this research during autumn months to get a full picture.

Comments

Comments are moderated to ensure respect towards the author and to prevent spam or self-promotion. Your comment may be edited, rejected, or approved based on these criteria. By commenting, you accept these terms and take responsibility for your contributions.

Disclaimer

The views, opinions, data, and methodologies expressed above are those of the contributor(s) and do not necessarily reflect or represent the official policies, positions, or beliefs of Greenbook.

ARTICLES

Top in Consumer Behavior

Partner Content

Your Claim Doesn't Live on a Survey Grid. It Lives on a Pack

Survey winners don’t always win on the shelf. Learn why testing claims on packaging reveals what truly drives shopper decisions.

Brent Snider

Managing Director of Global Business Development at Behaviorally

Partner Content

The Consumer in Your Segmentation Model May No Longer Exist

Traditional segmentation is losing relevance. Discover the rise of the Polyclass consumer and a more dynamic approach to understanding behavior.

Sam Killip

VP of Insights at Attest

Partner Content

GLP-1 Is Not Just Shrinking the Grocery Basket — It Is Reshaping It

GLP-1s are reshaping demand—less snacking, more protein. AI interviews reveal why behavior is shifting and what scanner data misses.

Dom Wong

CEO and Co-Founder at Pogo

From Behavioral Data to AI Commerce: Why the Consumer Journey Is Breaking (and Being Rebuilt)

Explore how AI, behavioral data, and agentic commerce are reshaping the consumer journey and what it...

Sign Up for

Updates

Get content that matters, written by top insights industry experts, delivered right to your inbox.