Categories

The Top 20 Most In Demand Supplier Types At IIeX NA 2017

At IIeX NA, 37 clients selected 102 unique suppliers for private meetings. What insights can we gain by analyzing those meetings?

IIeX North America was 2 weeks ago, and it was a resounding success on all levels. With 924 attendees in it’s 5th year it continues to grow year-on-year and attract the most diverse audience of stakeholders in the industry. That success can be attributed to a few factors, but primarily I believe it’s because the event is not simply a showcase for the best and brightest in the industry, but is also focused on connecting people: suppliers with investors, partners and clients.

One of the most important ways the event does that is via the IIeX Corporate Partner program. The gist is that client-side companies and/or investors review every attending supplier company who registers before the last few weeks of the event and can pick which firms they want to meet with in private meeting space we provide. There is no charge for anyone in this program: it’s simply a value add service we perform in order to help the cause. One of the fringe benefits is that we also get a fantastic view into what clients are looking for, and we get to share some of that information with the industry as a whole.

And that brings us to today’s post.

At IIeX a total of 37 organizations participated as Corporate Partners. The list of partners was:

- Amazon.com

- Bedford Systems LLC

- Big A** Solutions

- BMS

- Coca-Cola

- Constellation Brands

- Cox Communications

- Crossroads

- Delta Air Lines

- Discover Financial Services

- Eli Lilly & Co

- EO Products

- Facebook (Instagram)

- Georgia Pacific

- Harley-Davidson

- Hasbro

- Hershey’s

- Hulu

- Kantar (VC)

- Keurig

- Lowe’s

- Merck

- Navy Federal Credit Union

- P&G

- PepsiCo

- Sargento

- Schwans

- Securian Financial Group

- Southeastern Grocers

- St. Jude

- The Clorox Company

- Tillamook

- Vanguard

- Verizon Telematics

- Walmart

Those companies selected 102 unique Suppliers to meet with, for a total of 251 meetings (many suppliers were selected multiple times). That makes for a lot of happy attendees, but what insights can we glean from this?

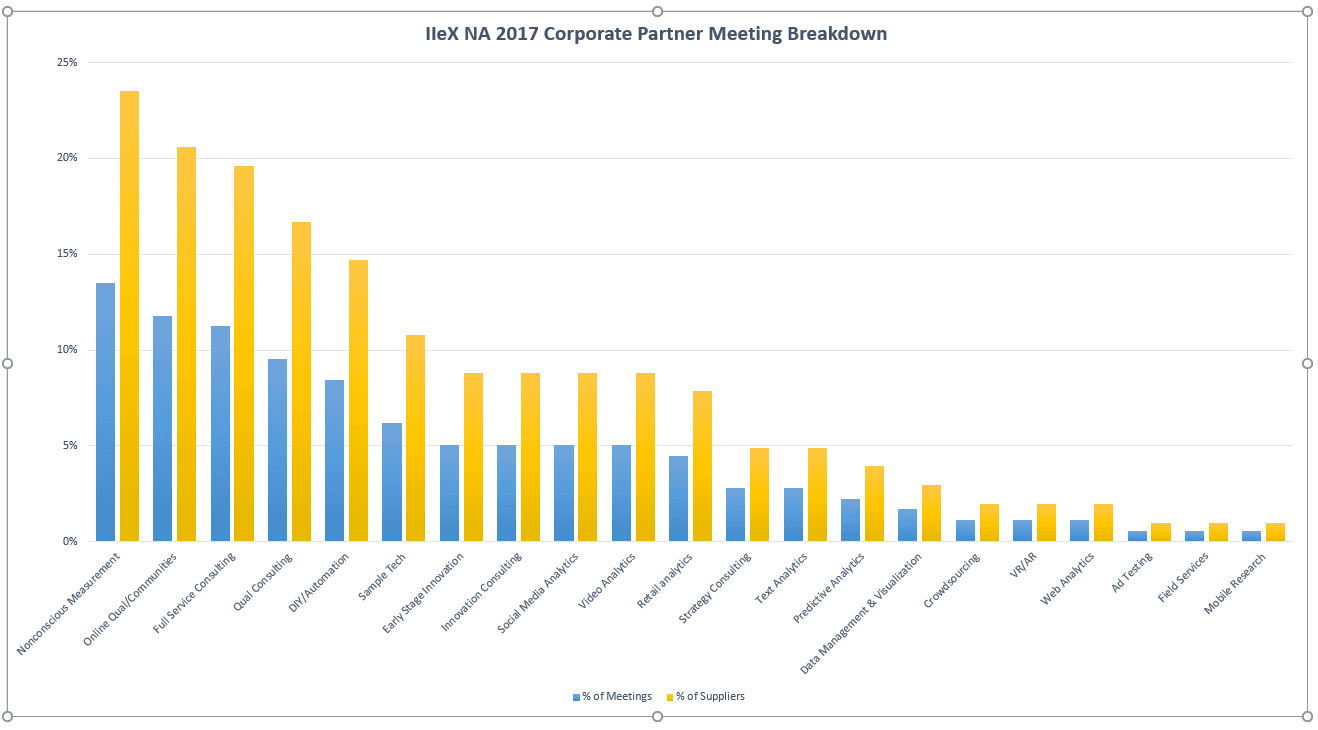

Here is a quick analysis of the percentage of meetings held by supplier category as well as percentage of category share within all meetings conducted.

Since the inception of the Corporate Program, the broad category of “Nonconscious Measurement” (which includes any research approach that is primarily based on neuroscience or behavioral science, including biometric and cognitive models) has led the pack, and this year was no different. Despite GRIT data indicating that these modalities have yet to reach saturation levels, clients continue to be focused on finding the right fit within their research priorities to incorporate these tools.

Rounding out the top 5 are online qual, full service, qual consulting and DIY/automation. You can see the entire list in the table below.

| Supplier Category | Meetings Scheduled |

| Nonconscious Measurement | 34 |

| Online Qual/Communities | 30 |

| Full Service Consulting | 28 |

| Qual Consulting | 24 |

| DIY/Automation | 21 |

| Sample Tech | 16 |

| Early Stage Innovation | 13 |

| Innovation Consulting | 13 |

| Social Media Analytics | 13 |

| Video Analytics | 13 |

| Retail analytics | 11 |

| Strategy Consulting | 7 |

| Text Analytics | 7 |

| Predictive Analytics | 6 |

| Data Management & Visualization | 4 |

| Crowdsourcing | 3 |

| VR/AR | 3 |

| Web Analytics | 3 |

| Ad Testing | 1 |

| Field Services | 1 |

| Mobile Research | 1 |

A few things jump out here, and the first is the surprising strength of qualitative (both tech and consultants). Historically qual has played a smaller role at IIeX as well as in share of project volume/budget globally but GRIT and ESOMAR have picked up high level indications that qual is growing on both fronts and we saw the demand at IIeX as well. I believe that the maturity of qualitative platform functionality combined with automation efficiencies, the ubiquity of consumer high-speed connectivity and video usage are a big part of this new interest. However, the prime driver is the need for insights organizations to get deeper connections and “why” based answers from consumers. Technology is now able to deliver on that need, hence the surging growth.

On a related note, another difference this time was the interest in general in full service organizations, albeit with a difference: all of the companies focus more on a consulting offering vs. a “big box research” position. Certainly the companies selected had some areas of specialization either methodologically or category/business issue wise, but all position themselves as strategic insights consultancies first.

DIY & Automation as well as Sample Tech were also much in demand indicating the continued strong interest in how automation of recruiting, data collection and reporting can help achieve organizational goals around speed and cost.

Rounding out the Top 10 (roughly), both Early Stage innovation tech and innovation consulting remain strong areas of interest and various types of analytics (most notably video and social media) were in demand as clients looked for new partners to help operationalize those data sources.

Surprisingly, VR/AR have declined, perhaps because the novelty has worn off in general, but likely because that tech, as cool and ripe with potential as they are, have yet to reach scale. I suspect as the grow in adoption on the consumer level and as suppliers achieve cost and speed efficiencies they will see a resurgence over the next few years.

Finally, mobile seems to have no become an afterthought: my view is that it is simply accepted as table stakes and is expected as a core capability just as generic online technology is. That makes sense from a methodological standpoint, but considering the challenges the industry still faces in adopting a “mobile foirst” design focus it will continue to be something that is discussed on stage even if clients are not making it an area of focus for partner selection.

All in all, this list should be a key datapoint for suppliers as they develop their strategies for the next 12-24 months and for clients to get a sense of where their colleagues in major companies are focusing their attention right now.

Comments

Comments are moderated to ensure respect towards the author and to prevent spam or self-promotion. Your comment may be edited, rejected, or approved based on these criteria. By commenting, you accept these terms and take responsibility for your contributions.

Disclaimer

The views, opinions, data, and methodologies expressed above are those of the contributor(s) and do not necessarily reflect or represent the official policies, positions, or beliefs of Greenbook.

More from Leonard Murphy

Patrick Comer on Building the Infrastructure Behind Modern Market Research

Patrick Comer discusses AI, research quality, synthetic data, leadership, and how Cint is shaping th...

Kristi Zuhlke: Stop Talking About AI and Start Building

Explore Kristi Zuhlke's practical approach to AI, synthetic consumers, and how insights teams can st...

Can AI Deepen Human Insight? Rhiannon Price on the Evolution of Qualitative Research

Rhiannon Price explores how AI is transforming qualitative research, empathy, and human insight in t...

From Panels to Behavioral AI: Vin DeRobertis on the Future of Insights

Generation Lab President Vin DeRobertis discusses behavioral data, AI, synthetic insights, and the e...

ARTICLES

Top in Insights Industry News

Qualtrics X4 and the New Questions Facing Insights Leaders

Qualtrics X4 2026 marked a pivot from AI hype to trust and action. Explore how insights leaders navigate synthetic research and the evolving role of j...

Karen Lynch

Chief Programming Officer at Greenbook

The Signal from QRCA 2026: AI Moderation is Good Enough, Sometimes

A decision matrix to choose AI-only, Hybrid, or Human-only based on risk, stakes, and nuance.

Karen Lynch

Chief Programming Officer at Greenbook

Follow the Spark: Why San Antonio Is The Place for Qual in February

At QRCA San Antonio, gain practical skills, peer insight, and new ideas to return to your work with clarity and renewed momentum.

Kristin Marino

Chair 2026 Conference at QRCA

Walmart Data Ventures and Data Quality Co-Op Redefine Authentic Insights

How Walmart’s Customer Spark Community Raises the Bar for Data Quality

Leonard Murphy

Chief Advisor for Insights and Development at Greenbook

{kind=link}

Sign Up for

Updates

Get content that matters, written by top insights industry experts, delivered right to your inbox.